- Direct

- Regular

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna.

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna.

- Performance

- Fund Facts

- Fund Specs

- Holdings

- Documents

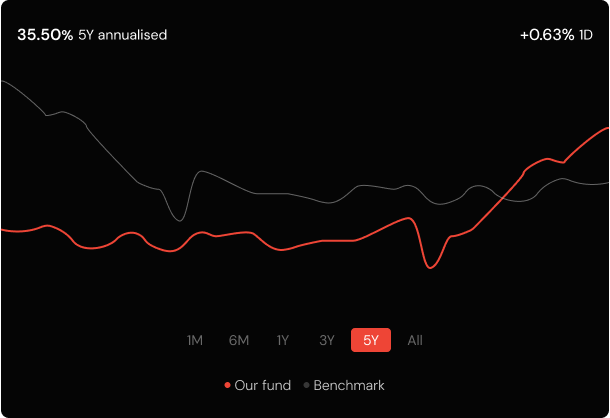

Performance

As on 30 Aug 2024As on 30 Sep 2024- Graph

- SEBI format table

Historical Returns (As per SEBI format)

| Our fund | BSE 250 Small Cap TRI ^ | BSE 250 Small Cap TRI # | ||||

|---|---|---|---|---|---|---|

| CAGR | Current Value | CAGR | Current Value | CAGR | Current Value | |

| 1 Year | 37.3% | ₹ 13,742 | 37.3% | ₹ 13,742 | 37.3% | ₹ 13,742 |

| 3 Year | 37.3% | ₹ 13,742 | 37.3% | ₹ 13,742 | 37.3% | ₹ 13,742 |

| 5 Year | 37.3% | ₹ 13,742 | 37.3% | ₹ 13,742 | 37.3% | ₹ 13,742 |

| since Inception | 37.3% | ₹ 13,742 | 37.3% | ₹ 13,742 | 37.3% | ₹ 13,742 |

| NAV / Index Value | ₹ 166.40 | ₹ 7,731 | ₹ 13,742 | |||

Date of allotment: Jun 15, 2024.

Period for which fund's performance has been provided is computed based on last day of the month-end preceding the date of advertisement

Different plans shall have a different expense structure. The performance details provided herein are of Direct Plan.

Since inception returns have been calculated from the date of allotment till August 30, 2024

Past performance may or may not be sustained in future and should not be used as a basis for comparison with other investments

Rolling returns have been calculated based on returns from regular plan growth option.

^ Fund Benchmark # Additional Benchmark

- Graph

- SEBI format table

Historical Returns (As per SEBI format)

| Our fund | BSE 250 Small Cap TRI ^ | BSE 250 Small Cap TRI # | ||||

|---|---|---|---|---|---|---|

| CAGR | Current Value | CAGR | Current Value | CAGR | Current Value | |

| 1 Year | 37.3% | ₹ 13,742 | 37.3% | ₹ 13,742 | 37.3% | ₹ 13,742 |

| 3 Year | 37.3% | ₹ 13,742 | 37.3% | ₹ 13,742 | 37.3% | ₹ 13,742 |

| 5 Year | 37.3% | ₹ 13,742 | 37.3% | ₹ 13,742 | 37.3% | ₹ 13,742 |

| since Inception | 37.3% | ₹ 13,742 | 37.3% | ₹ 13,742 | 37.3% | ₹ 13,742 |

| NAV / Index Value | ₹ 166.40 | ₹ 7,731 | ₹ 13,742 | |||

Date of allotment: Jun 15, 2024.

Period for which fund's performance has been provided is computed based on last day of the month-end preceding the date of advertisement

Different plans shall have a different expense structure. The performance details provided herein are of Direct Plan.

Since inception returns have been calculated from the date of allotment till August 30, 2024

Past performance may or may not be sustained in future and should not be used as a basis for comparison with other investments

Rolling returns have been calculated based on returns from regular plan growth option.

^ Fund Benchmark # Additional Benchmark

Fund Facts

As on 30 Aug 2024As on 30 Sep 2024This is an open ended hybrid fund that dynamically changes asset allocation.

- Scheme Code UMF/O/H/BAF/24/01/0006

- Inception Date 27 May 2024

- Allotment Date 15 June 2024

- Ideal Holding Period 2 Years+

- Lumpsum Minimum ₹50,000

- SIP Minimum Minimum Instalments - 6 Months ₹1,000

- Additional Purchase ₹1,000

Minimum

- Upto 12 months20% is free of charge, while the remaining 80% incurs the mentioned fees 2%

- Upto 2 years20% is free of charge, while the remaining 80% incurs the mentioned fees 1%

- Direct 0.92%

- Regular 1.39%

Level of Risk in the fund

Karthik

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod.

Aejas

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod.

This is an open ended hybrid fund that dynamically changes asset allocation.

- Scheme Code UMF/O/H/BAF/24/01/0006

- Inception Date 27 May 2024

- Allotment Date 15 June 2024

- Ideal Holding Period 2 Years+

- Lumpsum Minimum ₹50,000

- SIP Minimum Minimum Instalments - 6 Months ₹1,000

- Additional Purchase ₹1,000

- Upto 12 months20% is free of charge, while the remaining 80% incurs the mentioned fees 2%

- Upto 2 years20% is free of charge, while the remaining 80% incurs the mentioned fees 1%

- Direct 0.92%

- Regular 1.39%

Level of Risk in the fund

Karthik

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod.

Aejas

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod.

Fund Specs

As on 30 Aug 2024As on 30 Sep 2024- Morningstar Rating 5

- Inception Date Gold

- Asset Under Management ₹ 14,072.97 Cr

- Portfolio Turnover Ratio 0.25 last 12 months

- Modified Duration 2.66 Years

- Portfolio Macaulay Duration 2.81 Years

-

PRC MatrixShow

Credit Risk  Interest Rate Risk

Interest Rate Risk Relatively Low (Class A) Moderate (Class B) Relatively High (Class C) Relatively Low (Class l) Moderate (Class ll) Relatively High (Class lll) A-III IRR higher

CRR lowest -

Average Maturity (only for debt component)Show

Credit Risk Interest Rate Risk Relatively Low (Class A) Moderate (Class B) Relatively High (Class C) Relatively Low (Class l) Moderate (Class ll) Relatively High (Class lll) A-III IRR higher

CRR lowest -

Yield to MaturityShow

Credit Risk Interest Rate Risk Relatively Low (Class A) Moderate (Class B) Relatively High (Class C) Relatively Low (Class l) Moderate (Class ll) Relatively High (Class lll) A-III IRR higher

CRR lowest

- Morningstar Rating 5

- Inception Date Gold

- Asset Under Management ₹ 14,072.97 Cr

- Portfolio Turnover Ratio 0.25 last 12 months

- Modified Duration 2.66 Years

- Portfolio Macaulay Duration 2.81 Years

-

PRC MatrixShow

Credit Risk Interest Rate Risk Relatively Low (Class A) Moderate (Class B) Relatively High (Class C) Relatively Low (Class l) Moderate (Class ll) Relatively High (Class lll) A-III IRR higher

CRR lowest -

Average Maturity (only for debt component)Show

Credit Risk Interest Rate Risk Relatively Low (Class A) Moderate (Class B) Relatively High (Class C) Relatively Low (Class l) Moderate (Class ll) Relatively High (Class lll) A-III IRR higher

CRR lowest -

Yield to MaturityShow

Credit Risk Interest Rate Risk Relatively Low (Class A) Moderate (Class B) Relatively High (Class C) Relatively Low (Class l) Moderate (Class ll) Relatively High (Class lll) A-III IRR higher

CRR lowest

Holdings

As on 30 Aug 2024As on 30 Sep 2024Documents

As on 30 Aug 2024As on 30 Sep 2024-

Alternative NBFCs (Core Portfolio)

Robust & well managed Alt. NBFCs that cater to retail and MSME end-borrowers. We find superior risk-adjusted yields characteristics of securities rated AA- to BBB-.

-

Mid-Market Corporates

Robust & well managed Alt. NBFCs that cater to retail and MSME end-borrowers. We find superior risk-adjusted yields characteristics of securities rated AA- to BBB-.

-

Hybrid INVITs / REITs

Robust & well managed Alt. NBFCs that cater to retail and MSME end-borrowers. We find superior risk-adjusted yields characteristics of securities rated AA- to BBB-.

-

Liquid AAA, AA, A+ bonds / Cash

Robust & well managed Alt. NBFCs that cater to retail and MSME end-borrowers. We find superior risk-adjusted yields characteristics of securities rated AA- to BBB-.

-

Alternative NBFCs (Core Portfolio)

Robust & well managed Alt. NBFCs that cater to retail and MSME end-borrowers. We find superior risk-adjusted yields characteristics of securities rated AA- to BBB-.

-

Mid-Market Corporates

Robust & well managed Alt. NBFCs that cater to retail and MSME end-borrowers. We find superior risk-adjusted yields characteristics of securities rated AA- to BBB-.

-

Hybrid INVITs / REITs

Robust & well managed Alt. NBFCs that cater to retail and MSME end-borrowers. We find superior risk-adjusted yields characteristics of securities rated AA- to BBB-.

-

Liquid AAA, AA, A+ bonds / Cash

Robust & well managed Alt. NBFCs that cater to retail and MSME end-borrowers. We find superior risk-adjusted yields characteristics of securities rated AA- to BBB-.

Key Fund Principles

-

Avoid becoming too large too fast

We periodically close the fund to new subscriptions so ensure that client inflows do not outpace the borrowing demand from high-quality borrowers. We invest in shorter maturity bonds of fundamentally strong corporates at an attractive absolute yield. This protects us from having to forecast interest rates; a challenge that trips-up most professional investors most of the time. Equally important is the fact that short tenor also offers the enormous benefit of not having to predict the prospects of a business far into the future. Since uncertainties rise exponentially with time, we logically prefer to settle for a slightly lower yield than expose our capital to the risk of permanent loss due to potential disruptions over the longer term. We bear in mind that our upside is in any case capped by the bond's contracted yield, unlike the case of an equity investor who accepts long duration in the hope of earning an out-sized upside.

-

Avoid long ‘Duration’

We periodically close the fund to new subscriptions so ensure that client inflows do not outpace the borrowing demand from high-quality borrowers. We invest in shorter maturity bonds of fundamentally strong corporates at an attractive absolute yield. This protects us from having to forecast interest rates; a challenge that trips-up most professional investors most of the time. Equally important is the fact that short tenor also offers the enormous benefit of not having to predict the prospects of a business far into the future. Since uncertainties rise exponentially with time, we logically prefer to settle for a slightly lower yield than expose our capital to the risk of permanent loss due to potential disruptions over the longer term. We bear in mind that our upside is in any case capped by the bond's contracted yield, unlike the case of an equity investor who accepts long duration in the hope of earning an out-sized upside.

-

Think beyond credit ratings

We periodically close the fund to new subscriptions so ensure that client inflows do not outpace the borrowing demand from high-quality borrowers. We invest in shorter maturity bonds of fundamentally strong corporates at an attractive absolute yield. This protects us from having to forecast interest rates; a challenge that trips-up most professional investors most of the time. Equally important is the fact that short tenor also offers the enormous benefit of not having to predict the prospects of a business far into the future. Since uncertainties rise exponentially with time, we logically prefer to settle for a slightly lower yield than expose our capital to the risk of permanent loss due to potential disruptions over the longer term. We bear in mind that our upside is in any case capped by the bond's contracted yield, unlike the case of an equity investor who accepts long duration in the hope of earning an out-sized upside.

-

Embrace Illiquidity

We periodically close the fund to new subscriptions so ensure that client inflows do not outpace the borrowing demand from high-quality borrowers. We invest in shorter maturity bonds of fundamentally strong corporates at an attractive absolute yield. This protects us from having to forecast interest rates; a challenge that trips-up most professional investors most of the time. Equally important is the fact that short tenor also offers the enormous benefit of not having to predict the prospects of a business far into the future. Since uncertainties rise exponentially with time, we logically prefer to settle for a slightly lower yield than expose our capital to the risk of permanent loss due to potential disruptions over the longer term. We bear in mind that our upside is in any case capped by the bond's contracted yield, unlike the case of an equity investor who accepts long duration in the hope of earning an out-sized upside.